45% of AutoStore’s Revenue Comes From Existing Customers

Here’s a detailed financial analysis of the third-quarter financial results for 2024, based on the document:

1. Revenue and Order Intake

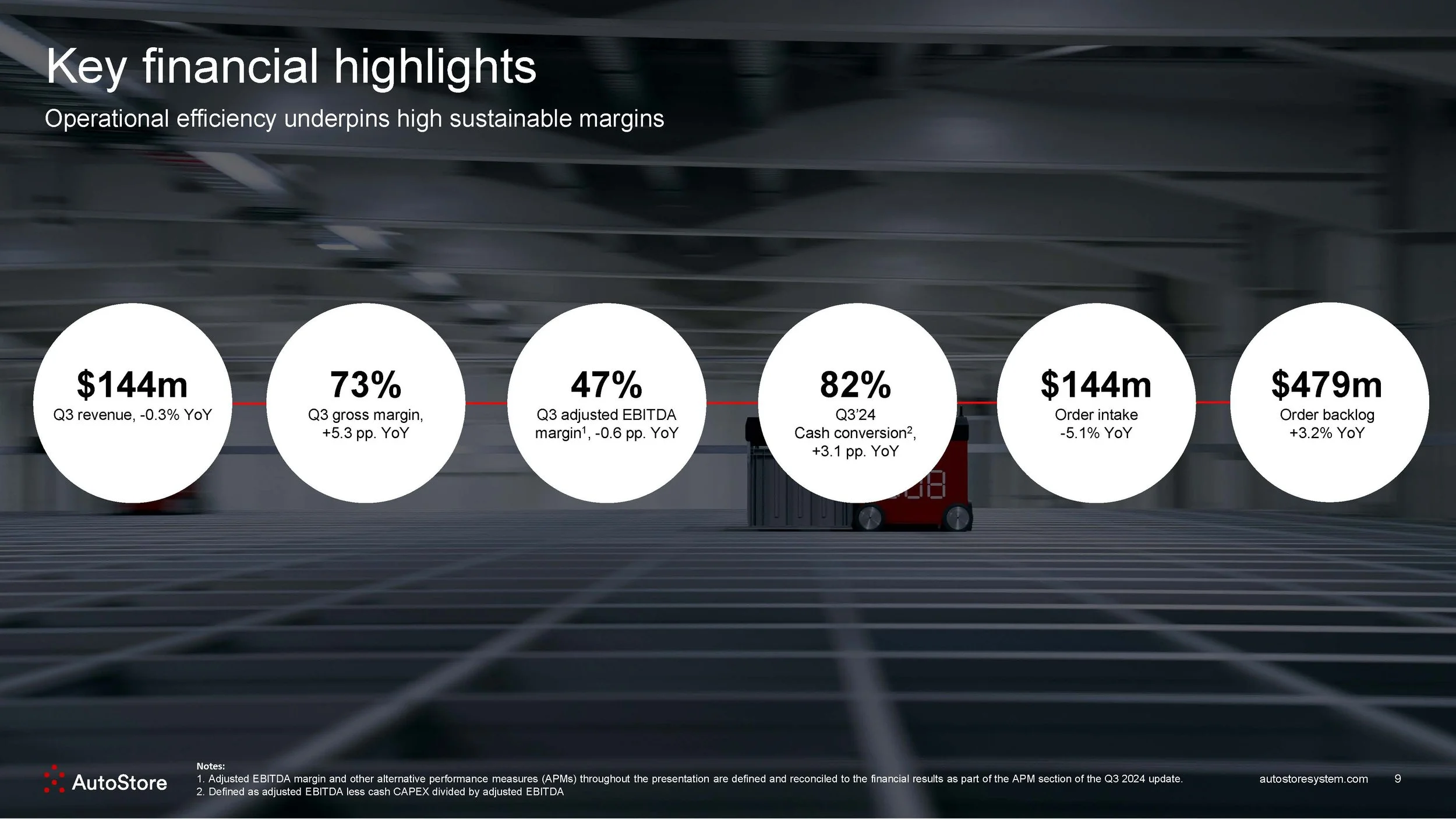

Revenue: $144.2 million for Q3, with a slight decrease of 0.3% YoY, but ahead of recent forecasts.

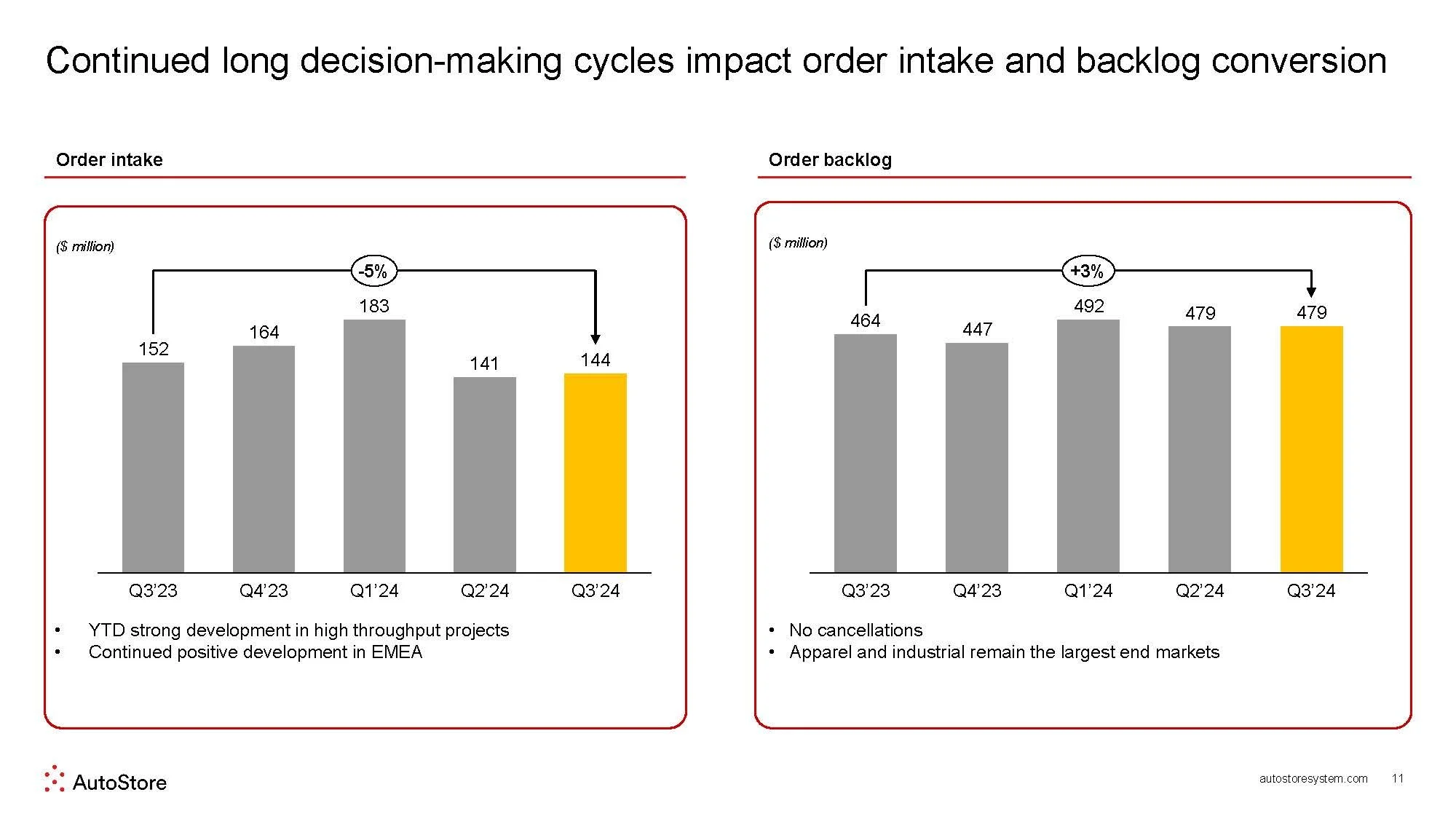

Order Intake: $143.9 million, reflecting a 5.1% decline YoY, while remaining consistent quarter-over-quarter.

Revenue by Region: Revenue contributions from EMEA, NAM, and APAC showed stability with EMEA experiencing the most consistent performance.

2. Margins and Profitability

Gross Margin: 73.5%, an increase of 5.3 percentage points YoY, signifying improved cost efficiencies and pricing stability.

Adjusted EBITDA Margin: 46.8%, a minor reduction of 0.6 percentage points YoY, sustained by cost discipline but slightly impacted by ongoing market challenges.

Free Cash Flow Conversion: High at 82%, showing efficient conversion of adjusted EBITDA to free cash flow, with minimal capex requirements relative to cash generation.

AUTOSTORE Earnings and Revenue Growth November 10th 2024

3. Backlog and Cash Flow

Order Backlog: $479 million, marking a 3.2% YoY increase, suggesting a strong pipeline but impacted by longer decision cycles in customer conversions.

Cash Position: Maintained at $280 million after key activities, with $26 million operating cash flow in Q3.

Lee Valley Tools has launched a new automated fulfillment center in West Ottawa that relies on automation and technology to increase efficiency and allow more room for manufacturing operations.

4. Segment Performance and Market Positioning

End-Market Diversification: The company serves various sectors, with Apparel & Sports (34%) and Industrials (17%) as major revenue contributors.

Customer Retention: Roughly 45% of revenue comes from existing customers, highlighting a stable customer base and recurring business.

5. Growth Drivers and Outlook

Long-Term Growth Projections: Light AS/RS (automated storage & retrieval system) market is projected to grow at a 14% CAGR to 2032, driven by global trends toward automation.

2024 Guidance: Full-year revenue guidance of $575-600 million has been reaffirmed, showing confidence in future order fulfillment and backlog conversion.

6. Strategic Initiatives and New Appointments

Operational Initiatives: New product developments target operational efficiency, including software and hardware enhancements like a multi-temperature solution and advanced control software.

Leadership Change: Keith White appointed as Chief Commercial Officer, effective November 12, 2024, which may strengthen commercial strategy and market reach.

Summary

Despite minor challenges in order intake and slight decreases in revenue, the company's profitability remains strong, underpinned by high gross and EBITDA margins. The backlog increase and cash position reflect stability and growth potential, while diversified end-market exposure mitigates sector-specific risks.

AutoStore Analysis from Yahoo Finance:

Positive Points

AutoStore Holdings Ltd (FRA:1IG) reported revenue of $144 million, slightly above the guided range of $135 million to $140 million.

The company maintained strong gross margins of 73.5% and adjusted EBITDA margins of 46.8%.

Appointment of Keith White as the new Chief Commercial Officer, bringing valuable experience from Hewlett Packard Enterprise and Microsoft.

Released new products, including an 18-level grid and multi-temperature solutions, enhancing storage density and system efficiency.

Strong cash position with $280 million, allowing continued investment in future growth.

Negative Points

Order intake was $144 million, showing a slight year-over-year decline and stagnation compared to the previous quarter.

The market remains challenging, with contraction observed over the past couple of years.

Sequential revenue decline reflects the current market environment affecting customer decision times.

Days Sales Outstanding (DSO) increased to over 70 days, indicating potential delays in customer payments.

Order intake remains flat sequentially, with a 5% decline from Q3 2023, indicating ongoing market challenges.

Q & A Highlights

Q: Can you provide more details on the regional performance, particularly why EMEA showed growth while North America and APAC did not?

A: Mats Vikse, CEO: The market remains challenging globally, but EMEA has shown more positive development compared to North America and APAC. This is not due to structural differences but rather a reluctance in decision-making in North America. Interest in automation remains high across all regions.

Q: Why has the Days Sales Outstanding (DSO) increased, and are there any concerns about delayed customer payments?

A: Paul Harrison, CFO: The project nature of our business causes timing fluctuations in receivables. We maintain a high-quality receivables book, and the increase in DSO is not indicative of payment delays.

Q: Can you discuss the current backlog and the share of projects scheduled for delivery next year?

A: Paul Harrison, CFO: The backlog is mostly less than 12 months old, with a significant portion scheduled for delivery next year. There have been no cancellations, indicating a healthy backlog.

Q: How sustainable are your current gross margins, and should we expect them to remain in the 70s?

A: Paul Harrison, CFO: We believe a gross margin starting with a seven is sustainable. While there are variables affecting gross margin, we expect it to remain in the 70s going forward.

Q: What are the main reasons for clients delaying orders, and how does this affect your growth strategy?

A: Mats Vikse, CEO: Delays are due to macroeconomic factors and lower volumes with customers, creating uncertainty. However, the interest in automation remains high, and less than 20% of warehouses are automated, indicating a significant growth opportunity.